[ad_1]

Investment banks and hedge funds including New York-based Och-Ziff are betting on the downfall of UK shopping centres, turning their attention to corporate bonds issued by one of the country’s largest retail landlords.

Bricks-and-mortar retailing in the UK is in crisis because of higher costs and consumers moving purchases online — trends that have forced a series of big retailers to enter insolvency arrangements, shutting thousands of stores.

Traders are building short positions against both the equity and bonds of Intu Properties, the owner of Manchester’s Trafford Centre, as it battles with falling rents and a heavy debt burden.

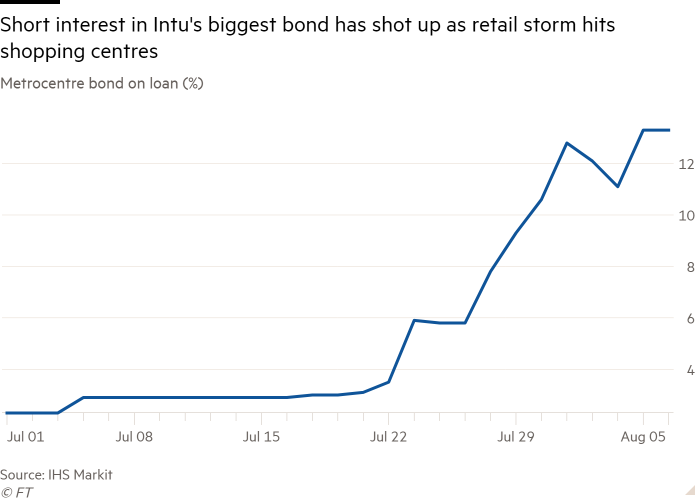

Short interest in Intu’s largest bond, a £485m security held against the Metrocentre in Gateshead, has more than quadrupled in one month, up from near 2.3 per cent on July 1 to more than 13 per cent on August 6, according to data provider IHS Markit.

Hedge fund Och-Ziff is one of those shorting the bonds, according to people familiar with the situation. Och-Ziff declined to comment.

Meanwhile, short interest in Intu’s free-floating shares remained at about a quarter of the company’s value since early July. London-based Odey Asset Management has a 3.3 per cent short position against Intu’s equity, data from the Financial Conduct Authority shows.

It is less common for investors to short bonds than equity, since debt is typically less volatile. The move to shorting Intu’s bonds reflects investor pessimism towards even the larger malls the company owns as a crisis sweeps the UK retail industry.

Intu, which owns £8.4bn of properties, said in half-year results last week that the business needed “radical transformation”.

The outlook for the FTSE 250 group’s Metrocentre bond, which is set to mature in 2023, was downgraded last week from stable to negative by rating agency Fitch, which cited shortfalls in rental income and the “more significant threat of recent retailer credit events”.

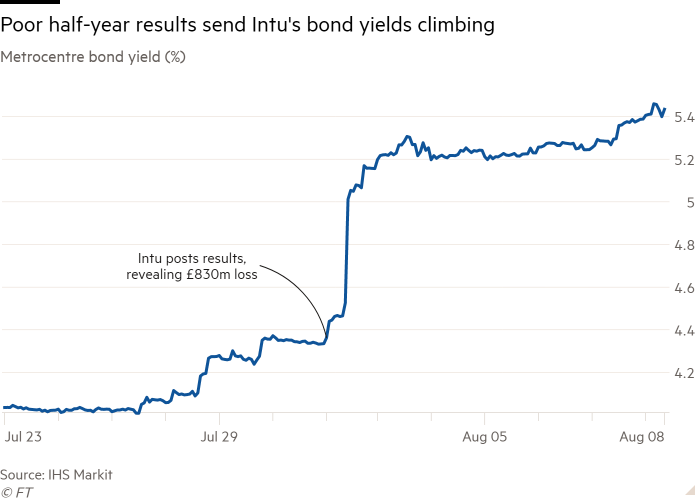

Intu’s results revealed a loss of £830m in the six months to June, nearly double the loss it made during the same period last year. The figures sent the company’s share price plunging and Intu shed half of its value in less than two weeks.

But the pain was not limited to its shares: yields on the Metrocentre bond have climbed 4 per cent since last Wednesday’s results to 5.44 per cent as investors sold the debt.

Robert Duncan, an analyst at Numis Securities, said short-sellers were betting that bond investors would lose more faith in Intu’s creditworthiness, pushing down the prices of its bonds. Intu will soon need to refinance much of its debt, he added: “The question is can they refinance on terms that will be economic for them?”

“The business is at a point where it’s cash burning,” said one credit trader who has short positions on Intu’s Metrocentre and convertible bonds. “There’s a structurally declining retail market and they’re sharing in its downside.”

Intu, whose largest shareholders are the property billionaire John Whittaker and his Peel Group, has faced a series of rent cuts and store closures from retailers such as House of Fraser, Debenhams and the Topshop owner Arcadia, which have entered insolvency arrangements over the past year.

Since 2015, the number of retailers opting for company voluntary arrangements, an agreement which allows a business to revise its debt with creditors, has doubled, according to PwC.

“The accumulation of CVAs makes it very difficult for rental growth to be extracted,” said Euan Gatfield at rating agency Fitch. “We don’t see any obvious green shoots that are likely to help turn the corner on the rental side.”

Miranda Cockburn, analyst at Panmure Gordon, said following Intu’s results that “the most pressing [challenge] is the high leverage . . . Looking at the individual properties, many are getting close to their loan-to-value covenants.”

Debt often comes with conditions on the value of the loan compared to the value of the property. If the value of the property falls, these so-called covenants can be breached, usually triggering an opportunity for the lender to impose new conditions or even take control of the asset.

Some of Intu’s borrowing is in a perilous state, with little space before hitting covenants.

The LTV covenant on debt against the group’s Uxbridge centre, which is owned jointly with the Malaysian pension fund Kumpulan Wang Persaraan, has 1 per cent headroom, while its Sprucefield centre in County Down has 3 per cent headroom, according to Intu’s figures.

“They have a lot of debt in lots of different boxes,” the credit trader said, adding: “By their annual results they’ll have tripped covenants in between four and six assets, which is crazy.”

If Intu’s properties drop 15 per cent in value, the group would have to stump up £83m to pay the covenant shortfall to lenders, Intu said in its results. The company declined to comment on the short interest in its shares and bonds.

Some traders had already cashed in their short positions against Intu’s shares: shorts peaked at a third in February, then dropped to 17 per cent in April.

But they have since risen to 25.4 per cent, indicating that traders expect further pain. Along with Odey, the hedge fund Marshall Wace is also shorting the stock. Both companies declined to comment.

Ms Cockburn said: “With the company becoming increasingly financially distressed, we . . . see no reason for investors to buy into Intu.”

[ad_2]

READ SOURCE